Robert Rodriguez of FPA Crescent recently gave a speech to the Institute of Private Investors. I highly reccomend paying attention whenever Robert Rodriguez speaks. He is right way more often than he is wrong.

Enjoy:

Caution Danger

Tuesday, February 28, 2012

Balestra Capital Q4 Letter

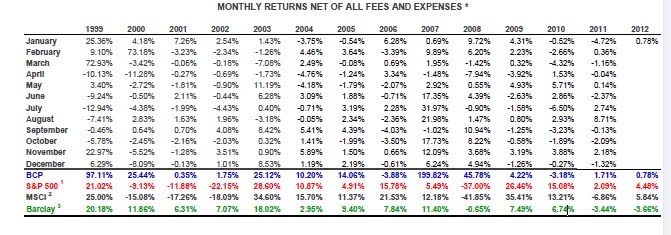

Balestra Capital is out with their Q4 letter (hat tip to Marketfoly). For those who are unfamiliar with Balestra, they were founded by James Melcher. They are a macro thematic fund, and Melcher was on the right side of the mortgage meltdown and has also been spot on with gold and some other prescient calls. His fund returned 1.71% in 2011 and has returned around 24.4% net since inception. His returns can be seen below:

His latest musings discuss his opinions on the markets, gold, etc.

Enjoy.

Balestra Capital on Gold & Inflation: Quarterly Newsletter

His latest musings discuss his opinions on the markets, gold, etc.

Enjoy.

Balestra Capital on Gold & Inflation: Quarterly Newsletter

Jeremy Grantham - GMO Capital Q4 2011 Letter

Jeremy Grantham of GMO Capital is out with his quarterly letter. The letter has three primary parts: 1. Standard Investment Adivce, 2. Tirade against the deficiencies of capitalism, and 3. Investment Observations for 2012. Personally my favorite part was the third part where he covered such topcis as inflation hedges (and their correlation), resource issues (a favorite topic of his), the current European situation, and a brief review of their prior predictions.

As usual the letter is worth reading. Enjoy.

GMO Capital - 2012.02.28

As usual the letter is worth reading. Enjoy.

GMO Capital - 2012.02.28

Monday, February 27, 2012

Titans at the Table - Jim Chanos, Jamie Zimmerman, Michael Novogratz, and Steve Kuhn

Jim Chanos, founder of Kynikos Associates, Jamie Zimmerman, CEO of Litespeed Management, Michael Novogratz, principal at Fortress Investment, and Steve Kuhn, head of fixed income trading at Pine River Capital Management were all on Bloomberg's new show Titans at the Table.

Overall the video was pretty interesting. Enjoy.

Overall the video was pretty interesting. Enjoy.

Thursday, February 23, 2012

Notes from UCLA Investment Conference

Ben Claremon posted his notes from the innagural UCLA investment conference. They can be found below. They are a little bit lengthy but overall worth skimming through. I personally liked Howard Marks discussion, although to be frank its nothing really new and very similar to his previous letters and book.

Enjoy.

2012 Anderson Investment Association Conference

Enjoy.

2012 Anderson Investment Association Conference

Sunday, February 19, 2012

Howard Marks latest Memo 2012

Below please find the latest out of Howard Marks of Oaktree Capital Management. In the memo he shares the lessons learned as the chairman of the Penn Endoment in the period of 2001-2010. While it is a bit similar to some of his past stuff, his past stuff is amazinng, so its worth reading.

Enjoy.

Howard Marks 2.15

Enjoy.

Howard Marks 2.15

Friday, February 10, 2012

Pershing Square's Presentation on Canadian Pacific

Hat tip to Markefolly for finding this. Pershing Square is out with their presentation on Canadian Pacific. It is quite detailed and worth looking through. He is taking a much more public and detailed approach than simply filing a 13D with a letter. He thinks the stock could be worth $140/share which is up from today's close of $74.63. So basically he thinks its a double from here in three years time, provided they get the right operator. Ackman is proposing an entire slate of directors to change the course of the company. Considering his success at Wendy's, McDonald's, General Growth Properties, Alexander & Baldwin, and of course JC Penney's.

Interesting stuff to say the least. Enjoy.

Pershing Square - 2012-02-06 - CP

Interesting stuff to say the least. Enjoy.

Pershing Square - 2012-02-06 - CP

T2 Partners January 2012 Letter

T2 Partners is out with their January 2012 monthly letter. For the month they returned 12.6%. Suffice it to say Whitney Tilson must be thrilled after a disasterous 2011. They were led by gains in NFLX, PBY, GS, REXI, and JCP.

The letter briefly discusses JCP and NFLX in the appendix.

Enjoy.

T2 Accredited Fund letter to investors-Jan 2012

The letter briefly discusses JCP and NFLX in the appendix.

Enjoy.

T2 Accredited Fund letter to investors-Jan 2012

Monday, February 6, 2012

Case Studies from Bruce Berkowitz of Fairholme Fund

In preperation for their big investor Q&A call on Wednesday. Bruce Berkowitz of Fairholme Fund has put out two case studies discussing why he thinks AIG and BAC are undervalued. He basically thinks they are worth more than 2x their current respective trading values.

Enjoy. (Note if for some reason you can see both and you are using Internet Explorer switch to Chrome or Firefox and you will be fine).

BAC:

120201 - Case Study I (With Disclaimers)

AIG:

120201 - Case Study II (With Disclaimers)

Enjoy. (Note if for some reason you can see both and you are using Internet Explorer switch to Chrome or Firefox and you will be fine).

BAC:

120201 - Case Study I (With Disclaimers)

AIG:

120201 - Case Study II (With Disclaimers)

Subscribe to:

Posts (Atom)